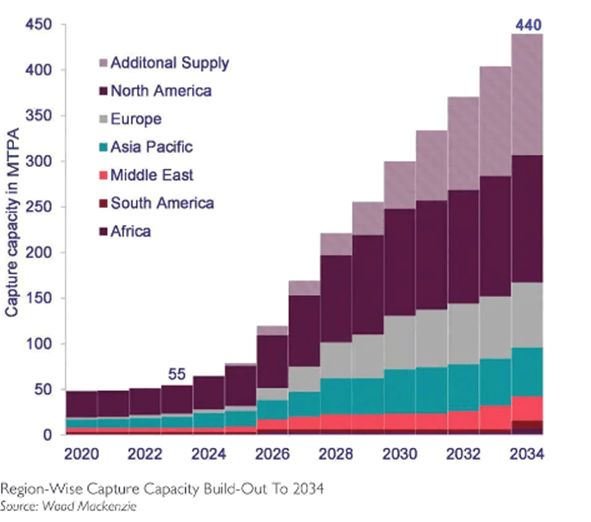

Carbon capture, utilization, and storage (CCUS) technology has had a rocky road. For the last twenty years, it has survived largely on government handouts. By 2020, the annual capacity was about 48 million tons per annum (MTPA). By the end of 2023, it had advanced to 55 MTPA.

But a new report from Wood Mackenzie predicts a massive surge over the next decade, when it will reach 440 MTPA. The North American market dominates, followed by Europe, Asia Pacific, and the Middle East.

Achieving the level of Carbon Capture projected by analysts requires almost $200 billion in funding. However, the business case for CCUS is such that Wood Mackenzie predicts that level of investment will materialize. Carbon Capture technologies will snare more than half of the cash with about 25% going to transport and 20% to storage.

According to Hetal Gandhi, CCUS Lead at Wood Mackenzie, the 2034 projections still fall short of the carbon capture needed by around 200 MTPA if decarbonization and net-zero targets are to be met.

“To deploy Carbon Capture at scale, heavy emitters must be motivated to decarbonize, the technology must be cost-effective and efficient, and a viable option for utilization or storage must be available,” she said. “The expected pace of CCUS deployment will be driven by the level of regulation and support in different countries.”

Government funding and incentives have made it easier for investors to gain confidence in achieving a return on their dollars. Around $80 billion in additional CCUS funding has been announced around the world, mostly in North America and the UK.

Technical challenges remain in moving captured carbon to where it can be stored as well as uncertainty over costs and permitting hurdles. Transport, too, is proving difficult and there have been recent leaks in carbon dioxide pipelines such as the Denbury Green Line in Louisiana earlier this year.

Some CCUS projects will store the gas. Others seek to transform it into a product or use it as part of enhanced oil recovery (EOR) in aging oil fields where production levels are faltering.

When you consider the money involved in building a CCUS project, the need for pipelines and storage repositories, and a slow payback over decades, a good portion of the projected CCUS investment may likely fall off. Unknown factors include fluctuations in the price of oil, gas, or power, geopolitical disruption, or the decarbonization push falling down the list of national priorities. Still, the CCUS build out will move ahead at a rapid pace.

“Predicting storage capacity and costs remains a challenge” said April Read, North American CCUS Subsurface Lead Analyst at Wood Mackenzie. “While the storage project pipeline continues to grow, operational project data and specific well information is sparse.

Requirements for these programs will be driven by regulations, many of which are still evolving or under development. This uncertainty favors making assumptions rather than predictions.”

Wood Mackenzie projects CO2 removal will need to scale up to 8 gigatonnes of annual capacity by 2050. But the current price tag of $30–1,000 per tonne of CO2 removed means net-zero goals will prove costly.

It remains to be seen how long the enthusiasm for CCUS remains, as many barriers stand in its way. In addition, a massive investment will need to be sustained for a quarter of a century to achieve decarbonization targets.