Solar power generation in 2023 set a new record according to analyst firm Wood Mackenze. As the numbers for 2024 are being crunched and finalized, it looks like 2024 was another banner year for solar.

Growth in 2024 was primarily in Texas, Florida, and California. As part of this, solar systems installed in businesses, schools, and government buildings rose by 13% in 2024, although residential solar new capacity fell for the year. EIA estimates that solar generated 27% more in 2024 than in 2023.

Wind’s year in the U.S. was not so impressive. New wind turbine capacity was the lowest in more than half a decade. However, wind generated 7% more electricity in 2024 compared to the previous year, accounting for almost 11% of the total electricity.

Meanwhile, the UK set a record for wind power generation in 2024 – 83 terawatt-hours (TWh) of electricity, up 4 TWh from 2023, according to the National Energy System Operator. Wind and solar now account for about a third of the nation’s electricity.

What does this mean for the future of gas turbine industry? Is there still a role for gas in an age of solar and wind power?

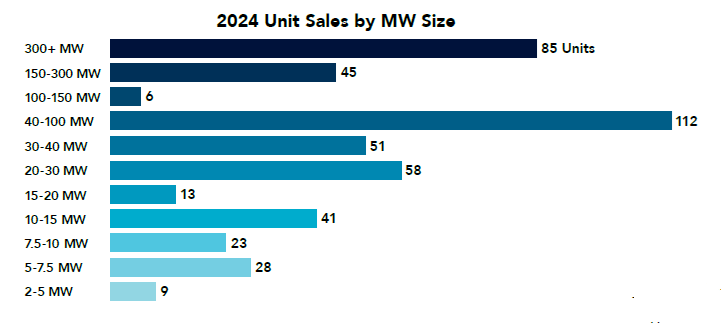

Intermittent energy sources require reliable, dispatchable, power to stabilize the grid, fulfill peak power needs, and offer backup when the sun doesn’t shine and winds don’t blow. Gas turbines are fulfilling this role. We see it in our data: our 2025 Global Gas Turbine Market Forecast reveals a surge in orders for gas turbines in the 30-100 MW range, and higher demand for fast-starting Aeroderivative gas turbines ideal to backup renewable power. In 2024, this range of power output grow to represent 34.6% of all gas turbine sales for the year.

Major OEM unit sales increased dramatically in 2024, and 2025 is building into another strong sales year. So strong, in fact, that order backlogs are increasing, with delivery times pushing out beyond the (typical) 18-36 month delivery time to 4-5 years on certain models. Factories are humming and working at capacity. To meet additional demand, GE Vernova has announced $600 million in investments to expand production facilities in the US.

But this bounty hasn’t been equally shared. At the smaller end of the market, units in the 1 MW to 5 MW range continue to lose market share to reciprocal engines. MAN Energy, with it’s smaller capacity units, will exit the gas turbine business to focus on their engine division. In addition, Solar Turbines has seen sales of it’s 1 MW Saturn unit evaporate, recording no orders for the past few years, as demand shifted to the 13 MW to 35 MW Titan Series of gas turbines (Titan 130, Titan 250, and Titan 350), which have seen sales almost double in the past 5 years.

Billion dollar babies

Tracking sales revenue, we account for genset-only (new gas turbine equipment) revenue, which does not include (among other things) packaging, delivery, or Long Term Service Agreements. Which makes the billion dollar revenue mark even more impressive. Each of the major OEMs have billion dollar babies/flagship units:

Mitsubishi Power’s M501J gas turbine sales revenue is expected to reach $1.5 billion in 2025. Sales of 19 units of this 330 MW Heavy Frame gas turbine, are expected in 2025.

GE Vernova’s (367 MW) Frame 7HA is projected to sell $1.2 billion this year, with sales of 15 units. Closely following, GE’s gangbuster (31 MW) Aeroderivative LM2500+, which has become the driver of North American LNG expansion, is expected to reach $1 billion in annual sales. Sales of 60 units are expected in 2025. We also anticipate the LM2500+ will become GE Vernova’s largest revenue unit over the next 10 years. With it’s 5-min fast-start capabilities, operators are purchasing multiple units to support peaking power in markets witnessing renewable expansion.

Siemens Energy’s flagship SGT-800 unit (rated at 62 MW) is expected to reach $1.2 billion in annual equipment revenue. Almost 40 unit sales per year are expected.

Growing market, greater opportunities

The overall market is expected to reach $16.1 Billion in annual equipment sales (new gas turbine units), up from $14.6 billion in 2023. Used equipment and older units will benefit from the growing order backlog, forcing operators to squeeze a bit more life out of their older units, driving increasing demand in parts and Aftermarket Services. Overhaul and Maintenance revenues increased last year to $59.1 Billion.

The market is HOT. Sales are increasing. To find out where opportunities are and what’s driving new business over the next 5-10 years, order your copy of the 2025 Gas Turbine Market Forecast.